CBI Index 2025Q2 Released by the National School of Development, Peking University

China Online Consumer Brand Index (CBI) (2023-2025Q2)

Encouraging innovation and healthy competition is essential for achieving high-quality development. The “China Online Consumer Brand Index” is the first online consumer index dedicated to benchmarking high-quality development. This index was jointly developed by the National School of Development at Peking University, the Digital Finance Research Center at Peking University, and the Business School of Sun Yat-sen University, with support from Alibaba’s Taobao and Tmall Group.

This index comprehensively measures consumption quality and brand equity based on underlying metrics such as sales, prices, search volume, and customer reviews. Leveraging big data, it evaluates brands’ equity and tracks changes in consumption quality through the average score of a “basket” of consumer brands. It complements traditional macroeconomic indicators like total retail sales and the consumer price index (CPI) by adding the quality dimension of consumption. Additionally, it provides valuable insights to guide brand development and business strategies in the China market.

The CBI Index has three components:

(1) China Online Consumer Brand Index (CBI): This captures the average consumption quality levels across different product categories in prefecture-level cities.

(2) China Online Brand Purchase Index (BPI): This highlights the relative purchasing power for top-rated brands across prefecture-level cities.

(3) China Top 500 Online Consumer Brands List (CBI500): This ranks the top 500 online consumer brands entirely based on actual consumer purchasing behaviors, intending to guide brand’s development and promote healthy competition in the e-commerce market. This quarter, a special study of the Fast-Moving Consumer Goods Top 50 Emerging Brands List, has been added. It focuses on analyzing new brands with more recent founding years, rapid growth, and demonstrated innovation capabilities.

Brand Rating and Index Methodology

As the world’s largest online retail market, China’s e-commerce market not only creates new opportunities for brand development but also serves as a dynamic basis for macroeconomic analysis.

The CBI leverages big data from online consumption. Brand ratings are derived from multiple online consumption metrics, with higher scores indicating higher quality, stronger consumer preference, and growth potential. The top-performing brand in each product category is standardized to a score of 100, while unbranded products receive a score of 0. The CBI is the average rating of a “basket” of consumer brands, with higher scores indicating higher overall consumption quality. The total score of this same “basket” corresponds to another index, the BPI, where higher scores represent stronger purchasing power. By limiting the “basket” of brands to specific quarterly time frames, sectors, or regions, it becomes possible to generate indexes for particular time frames × product categories × region combinations.

The scoring system evaluates four key dimensions: Brand Awareness (32.5%), Brand Novelty (27.5%), Customer Loyalty (22.5%), and Customer Satisfaction (17.5%), encompassing a total of 12 underlying metrics. The relative weights of these dimensions are determined using a subjective weighting method, where an expert panel independently assigns weights, and the average of their evaluations is used as the final weighting. Within each dimension, the relative weights of individual metrics are calculated using the coefficient of variation method.

Brand Novelty is a metric typically not included in traditional rating systems but has the second-highest weighting in our brand rating system. This reflects a focus on identifying brands demonstrating rapid growth, strong appeal to younger consumers, and a commitment to product innovation. The approach is especially favorable to emerging brands that are creative, which resonates with the dynamic nature of China’s e-commerce market.

Trend Analysis

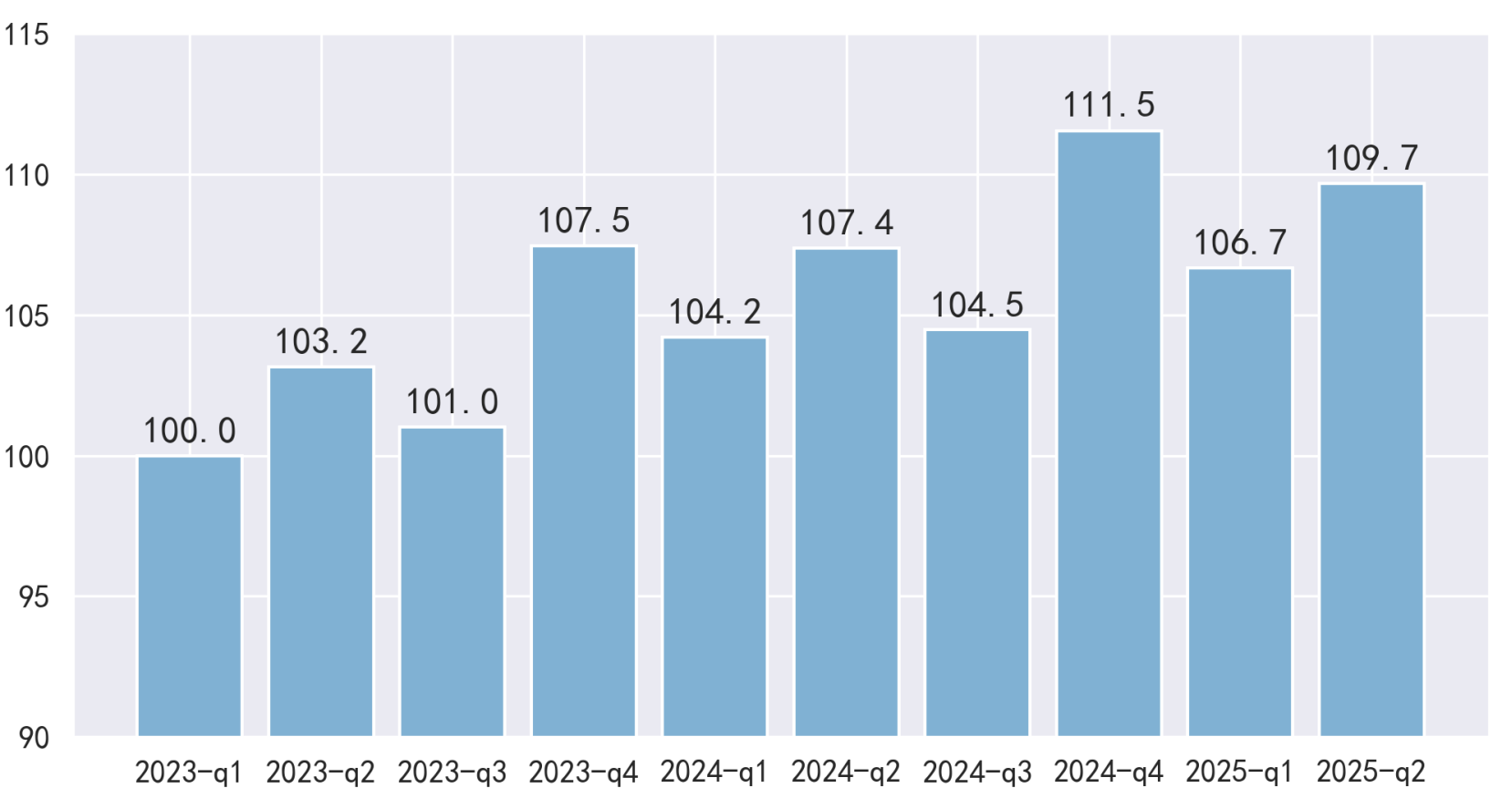

In the second quarter of 2025, the CBI continued to rise, increasing from 63.38 in Q1 2025 to 65.21 in Q2 2025. CBI data tends to peak in the second and fourth quarters, corresponding to the quarters of the “6.18 Shopping Festival” and ”11.11 Shopping Festival.” During these periods, consumers are more likely to purchase high-quality brands rather than low-cost generic brands. This phenomenon can be attributed to two main reasons: First, consumers have developed stable expectations for shopping festivals. Most premium brands strategically offer consumer benefits during these festivals and revert to their original pricing afterward. Such adjustments are unlikely to create a negative perception of “persistent price cuts,” allowing consumers to maintain a consistent perception of the brand’s premium image. Rational consumers are thus motivated to take advantage of these events to fulfill their purchasing needs. Second, China is transitioning from an “upper-middle-income country” to a “high-income country,” a process often accompanied by an increase in the consumption rate and an upgrade in consumption quality. When unbranded goods, low-end goods, and premium brand goods all participate in promotional discounts, the relative sales of premium brands see a greater increase.

To control for the impact of the 6.18 Shopping Festival on second-quarter data, a comparison with 2024Q2 shows that the CBI grew by 2.21% year-on-year, continuing the growth trend in brand consumption observed since 2023. If the first quarter of 2023, the starting period of the initial report, is set as the base period with an index value of 100, then subsequent values can be calculated relative to this baseline. Based on this calculation, the second quarter of 2025 saw an increase of 9.7% compared to the base period index.

Figure 1. CBI

(Using Q1 2023 as the Base Period, Base Index = 100)

Industry Comparison

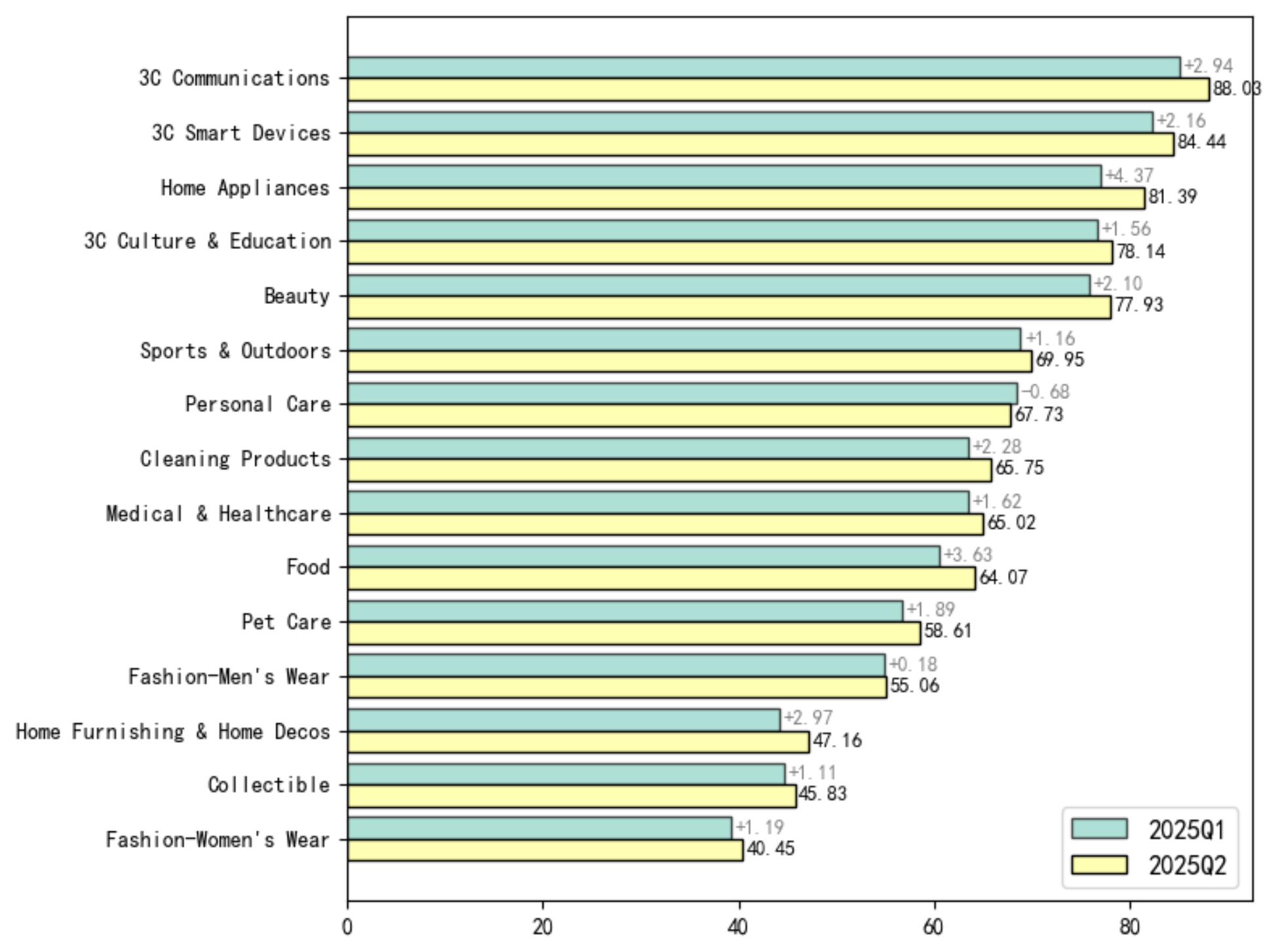

The CBI shows significant differences in both absolute values and growth dynamics across industry categories. A higher CBI indicates a greater concentration of sales among leading brands and fewer unbranded products, while a lower CBI suggests an opportunity for brands to enter and compete. When an industry’s CBI shows an upward trend, it signals either the gradual formation of leading brands or sales consolidation among existing leading brands.

Consistent with Q1, 3C (mobile phones, smart devices and other digital products), home appliances, beauty products, and sports & outdoors exhibit higher CBI values. In these industries, consumers have higher demands for product quality and functionality, along with a stronger sense of brand awareness. Industries with higher quarter-on-quarter CBI growth include home appliances, food, and home furnishing & home decos. The significant growth in home appliances could be attributed to government subsidies and the 618 Shopping Festival, though its year-on-year growth is less pronounced. The food industry experienced notable growth due to traditional holidays in Q2, such as the Qingming Festival and Dragon Boat Festival, which boosted consumption of festive foods. Meanwhile, the growth in the home furnishing & home decos industry has been fueled by the continued positive impact of logistics development on large-item consumption, as well as ongoing innovation from leading brands.

Figure 2. Comparison of CBI by Industry Category

Regional Analysis

In terms of regional rankings, the CBI shows that the top ten cities are predominantly second- and third-tier cities, such as Hefei in Anhui Province, Huai’an in Jiangsu Province, Zhengzhou in Henan Province, and Nanchang in Jiangxi Province. However, emerging first-tier cities, including Nanjing, Hangzhou, and Wuhan, stood out in Q2 with higher average consumption quality. For the BPI, first-tier cities like Beijing, Shanghai, Guangzhou, and Shenzhen continue to dominate the top rankings. The remaining top ten cities are mostly emerging first-tier cities. Across both dimensions—CBI and BPI—three cities, Hangzhou, Wuhan, and Nanjing, consistently ranked in the national top ten. This highlights the strong growth potential of emerging first-tier cities.

Table 1: Top Ten Cities in the Brand Index Series

|

Newest: 2025Q2 |

Comparison: 2025Q1 |

||

|

CBI Top 10 (Q2 2025) |

BPI Top 10 (Q2 2025) |

CBI Top 10 (Q1 2025) |

BPI Top 10 (Q1 2025) |

|

Hefei |

Shanghai |

Hefei |

Shanghai |

|

Zhengzhou |

Beijing |

Zhengzhou |

Beijing |

|

Nanjing |

Hangzhou |

Huai'an |

Hangzhou |

|

Nanchang |

Shenzhen |

Nanchang |

Guangzhou |

|

Huai'an |

Guangzhou |

Nanjing |

Shenzhen |

|

Hangzhou |

Chengdu |

Zhoukou |

Chengdu |

|

Wuhan |

Suzhou |

Huaibei |

Suzhou |

|

Linyi |

Chongqing |

Yancheng |

Chongqing |

|

Huaibei |

Wuhan |

Kaifeng |

Wuhan |

|

Zhoukou |

Nanjing |

Linyi |

Nanjing |

The top five brands in the rankings are Apple, Midea(美的), Xiaomi(小米), Haier(海尔), and Huawei(华为). Midea and Haier, boosted by strong summer demand for air conditioners, rose from fourth and fifth in Q1 to second and fourth in Q2. Xiaomi, with a diversified strategy spanning multiple industries and a focus on smart home products like air conditioners, held steady in third place. The impact of summer consumption was particularly evident in Q2, with brands like Beneunder(蕉下), Ulike, and Crocs experiencing significant performance boost.

Other fast-growing brands fall into three key categories: First, the electric vehicle market is evolving from localized operations to a unified national market, with a focus on standardization and smart technology. As smart commuting becomes more popular and instant commerce and delivery services expand, the demand for two-wheeled electric vehicles has increased significantly. Long battery life, lightweight designs, and intelligent features have become the main trends, driving the rise of brands like Niu(小牛电动) and ZEEHO(极核). Second. The liquor industry’s shift toward lower alcohol content and a younger demographic has fueled strong growth for brands like JianNanChun Chiew(剑南春) and Luzhou Laojiao(泸州老窖). Third, with expanded government subsidies and the 618 Shopping Festival, home improvement brands such as SKSHU Paint(三棵树) and Dongpeng Tiles(东鹏瓷砖) have leveraged efficient online and offline subsidy redemption systems to boost growth. These government incentives have been instrumental in driving their success.

Table 2: CBI500 (Top 50)

|

Rank |

Brand |

Category |

|

|

1 |

苹果 |

Apple |

3C Digital |

|

2 |

美的 |

Midea |

Home Appliances |

|

3 |

小米 |

Xiaomi |

3C Digital |

|

4 |

海尔 |

Haier |

Home Appliances |

|

5 |

华为 |

HUAWEI |

3C Digital |

|

6 |

联想 |

Lenovo |

3C Digital |

|

7 |

耐克 |

NIKE |

Sports & Outdoors + Fashion |

|

8 |

源氏木语 |

YESWOOD |

Home Furnishing & Home Decos |

|

9 |

李宁 |

LI-NING |

Sports & Outdoors + Fashion |

|

10 |

阿迪达斯 |

adidas |

Sports & Outdoors + Fashion |

|

11 |

斐乐 |

FILA |

Sports & Outdoors + Fashion |

|

12 |

珀莱雅 |

PROYA |

Beauty |

|

13 |

茅台 |

Moutai |

Food |

|

14 |

欧莱雅 |

L’ORÉAL |

Beauty |

|

15 |

优衣库 |

UNIQLO |

Sports & Outdoors + Fashion |

|

16 |

剑南春 |

JianNanChun Chiew |

Food |

|

17 |

维沃 |

vivo |

3C Digital |

|

18 |

格力 |

Gree |

Home Appliances |

|

19 |

兰蔻 |

LANCÔME |

Beauty |

|

20 |

蕉下 |

Beneunder |

Sports & Outdoors + Fashion |

|

21 |

林氏家居 |

LINSY |

Home Furnishing & Home Decos |

|

22 |

安踏 |

ANTA |

Sports & Outdoors + Fashion |

|

23 |

索尼 |

SONY |

3C Digital |

|

24 |

泡泡玛特 |

POP MART |

Collectible |

|

25 |

/ |

OPPO |

3C Digital |

|

26 |

雅诗兰黛 |

ESTĒELAUDER |

Beauty |

|

27 |

无印良品 |

MUJI |

Household Items |

|

28 |

华硕 |

ASUS |

3C Digital |

|

29 |

大疆 |

DJI |

3C Digital |

|

30 |

周大福 |

Chow Tai Fook |

Jewelry & Accessories |

|

31 |

爱他美 |

Aptamil |

Food |

|

32 |

/ |

Babycare |

Household Items |

|

33 |

五粮液 |

Wuliangye |

Food |

|

34 |

领丰金 |

LING FENG GOLD |

Jewelry & Accessories |

|

35 |

公牛 |

BULL |

Home Furnishing & Home Decos |

|

36 |

海蓝之谜 |

LA MER |

Beauty |

|

37 |

得力 |

deli |

Office & School Supplies |

|

38 |

回力 |

Warrior |

Sports & Outdoors + Fashion |

|

39 |

维达 |

Vinda |

Household Items |

|

40 |

雀巢 |

Nestlé |

Food |

|

41 |

猫人 |

MiiOW |

Sports & Outdoors + Fashion |

|

42 |

由莱 |

Ulike |

Medical/Healthcare/Nutritional Products |

|

43 |

泸州老窖 |

Luzhou Laojiao |

Food |

|

44 |

百丽 |

BELLE |

Sports & Outdoors + Fashion |

|

45 |

苏泊尔 |

SUPOR |

Home Appliances |

|

46 |

伊利 |

Yili |

Food |

|

47 |

斯维诗 |

Swisse |

Medical/Healthcare/Nutritional Products |

|

48 |

佳能 |

Canon |

3C Digital |

|

49 |

荣耀 |

HONOR |

3C Digital |

|

50 |

美素佳儿 |

Friso |

Food |

This quarter’s index series highlights several key trends: Online consumption of high-quality brands in China continues to grow steadily. In terms of industries, 3C digital products, home appliances, beauty, and sports & outdoor lead in CBI scores, while home appliances, food, and home improvement & furniture are the fastest-growing sectors this quarter, driven by factors like government subsidies, traditional festivals, and improved logistics. Regionally, emerging first-tier cities such as Hangzhou, Wuhan, and Nanjing stand out with stronger brand purchasing power and higher average consumption quality. On the brand rankings, companies embracing industry transformation are growing the fastest, including lightweight and intelligent electric vehicle brands and liquor brands targeting younger consumers. These findings provide valuable insights into China’s consumption trends and offer guidance for driving brand innovation and growth.

Attached:China Online Consumer Brand Index(2023-2025Q2)Full Report

Attached:CBI500 (2025Q2)