December 13th, 2009

Author: Yiping Huang, ANU and Peking University

China's current account surplus has been the subject of fierce debate in recent times, with politicians in the United States and Western Europe often criticising China's rigid exchange rate regime. Their real focus, however, was probably not the exchange rate policy per se, but China's growing trade and current account surpluses. It has been argued that, by artificially depressing the value of the renminbi (RMB), China took jobs away from its trading partners.

<IMG class="aligncenter size-full wp-image-8528" title="A woman walks past a foreign exchange store that accepts renminbi (RMB). (photo: Reuters)" height=252 alt="" src="

/en/userfiles/Image/2010-05/R_20100521094935497.JPG

" width=400>

Recently, some American policymakers have again blamed China for helping cause the subprime crisis in the U.S; an accusation that was rejected strongly by Chinese policymakers.

But Chinese economists and government officials have also grown uneasy about the rapidly expanding external sector imbalances. Persistent current account surpluses have meant that China, as a low-income economy, has been exporting capital to rich countries. Rising external surpluses have often worsened China's trading relations with its major trading partners.

For the past several years at least, the Chinese government has made improving the quality of growth a top policy priority. It has made various efforts to limit export growth and narrow current account surplus, by lowering export tax rebates, liberalizing import barriers and increasing exchange rate flexibility.

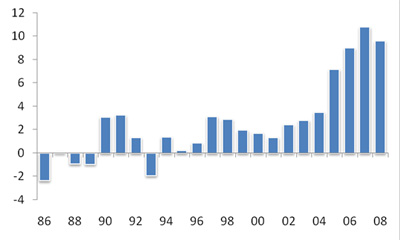

Rapid growth in China's current account surplus is, in fact, a relatively recent phenomenon. During the second half of the 1980s, China maintained persistent trade and current account deficits (see Chart 1).

The sharpest rise in current account surplus occurred after 2004. Within three years, the surpluses jumped from 3.5 per cent of GDP in 2004 to 10.8 per cent in 2007. In 2008, external demand was severely cut by the global crisis. But China's current account surplus still stood at 9.6 per cent of GDP.

Chart 1. China's Current Account Balances, 1986-2008 (% GDP)

<IMG class="aligncenter size-full wp-image-8526" title=Yiping_Chart1 height=240 alt="" src="

/en/userfiles/Image/2010-05/R_20100521094937280.jpg

" width=400>

Source: CEIC Data Company.

What are the fundamental factors contributing to China's growing current account surpluses? Previous explanations may be grouped into five broad categories:

? Measurement errors: The so-called ‘hot money' inflows disguised in forms of export revenues or income transfers probably exaggerate the current account surplus;

? Saving and investment gap: The extraordinarily high saving rate, which is determined by various economic and cultural factors, results in a large saving-investment gap and, therefore, massive current account surplus;

? Industry relocation: Relocation of industries from other East Asian economies to China in recent years also transfers trade surpluses from these economies to China;

? By-product of policies promoting growth: The government policies promoting exports and GDP growth and pursuing full employment boost domestic production and external surpluses; and

? Exchange rate distortion: An undervalued currency raises exports and depresses imports, and thus inflates China's trade surplus.

All these explanations are helpful for understanding China's growing external imbalance problem. However, the saving and investment gap hypothesis is really an identity. Some analysts tried to attribute the high saving ratio to Chinese cultural tradition. But the fact is that China ran current account deficits or small current account surplus in most years during the reform period.

The by-product hypothesis and the industry relocation hypothesis are sound reasons behind the changing current account position. But it is difficult to yield actionable policy prescriptions to remedy the problem based on such analysis.

And finally, the exchange rate hypothesis, while uncontroversial, doesn't offer practical policy responses. Empirical studies have failed to confirm that current account imbalances are correlated with exchange rate regimes. Perhaps a sharp appreciation of the nominal exchange rate could ameliorate the problem, but that does not look like a feasible policy option, at least in the short term, at it is a remedy that does not go to heart of the long run structural problem behind China's current account surpluses.

Here, we suggest an alternative hypothesis: factor market distortion and associated producer subsidy equivalent as a result of China's asymmetric market liberalization approach is the core problem.

During the reform period, the government focused on reform of the product markets, including abandoning policy interventions in domestic markets and liberalizing trade in goods and services. Today, the prices of more than 95 per cent of products are determined in free market forces.

In contrast, factor markets remain highly distorted.

China is known for the low cost and abundance of its labour, which has been a key factor behind China's success in labour-intensive manufacturing exports. But labour costs in China may be distorted, for two interrelated reasons – segmentation of rural and urban labour markets and under-development of social welfare systems.

Labour market segmentation has largely been a result of the household registration system (HRS) introduced in the pre-reform period, though the effectiveness of this system has weakened in recent years. Today, HRS no longer prohibits labour mobility, but it is still an important institutional discrimination against migrant workers, who normally receive only half or even one-third of what their urban cousins receive for performing the same job functions.

Distortions in capital markets exist at two levels. Domestically, the financial system remains repressed, evidenced by highly regulated interest rates and state influences on credit allocation. Externally, capital account controls are more restrictive on outflows than on inflows. The currency is likely undervalued, and has probably been so for the past 15 years.

China's financial system, especially its banking sector, has undergone major transformation. But financial intermediation remains overly dependent on banks, especially the large state-owned commercial banks (SOCBs). Despite significant reform, most large banks are still majority-owned by the state and their top executives still appointed by the government.

China still maintains interest rate regulation. Despite numerous reforms, giving banks more flexibility in determining the actual rates, the People's Bank of China (PBOC) still maintains floors for lending rates and ceilings for deposit rates.

The larger gap between nominal GDP growth potential and long-term government bond yields in China, relative to the gaps in other Asian economies, also suggest that China's capital is far too cheap. Compared with other Asian economies, China's nominal growth potential is among the highest, but its Treasury yield is among the lowest.

The price of key energy products, such as oil, gas and electricity, are also regulated by the state. Often when international energy prices grow rapidly, domestic prices would lag significantly in order to avoid shocks to domestic production and consumption. For instance, oil prices peaked at nearly $150 per barrel in 2008, the corresponding domestic prices were only around $80.

China has introduced a series of environmental laws and regulations. However, they have not been well-enforced, and environmental degradation in China has contributed to global climate change, as well as regular droughts in Northern China and frequent floods in Southern China.

According to a joint study by the National Bureau of Statistics (NBS) and the State Agency for Environmental Protection (SAEP), an incomplete count of costs of environmental damage amounted to about 3.05 per cent of GDP in 2004.

Cost distortions in the above five categories add up to RMB2,138 billion in 2008, or 7.2 per cent of GDP. Clearly, the environment and capital are by far the largest areas of cost distortions. Leaving year-to-year variations aside, it is clear that producers in China receive significant ‘subsidies' from the rest of the economy, equivalent to about 7 per cent of GDP or 15 per cent of industrial GDP.

Such producer subsidy equivalent (PSE) lowers input costs, increases production profits, raises investment returns and improves international competitiveness of the Chinese exports. It therefore makes China growth very strong, averaging 10 per cent a year during the past thirty years. But it makes investment and exports even stronger. This is the fundamental cause of the imbalance problems facing China: too much investment and too much export.

Meanwhile, the PSE depresses household income. Total labour compensation dropped from 52 per cent of GDP in 1997 to only 40 per cent in 2007. This was the fundamental cause of sluggish consumption: if household income share of GDP declines over time, consumption growth would not be able to keep up pace with GDP growth.

Too much exports and too weak consumption were probably the most important factors behind China's large current account surpluses. Therefore, while exchange rate policy is important, it is not the only or perhaps the most important part of the story. Exclusive focus on exchange rate policy issue is not likely to be productive in terms of dealing with the imbalance problem, economically or politically.

The factor market distortion hypothesis not only satisfactorily explains the imbalance but also provides a clear set of policies for remedying the problem: liberalizing the factor markets. These should include the abolition of the HRS, better enforcement of employers' social welfare contribution, the introduction of market-based interest rates, an increase in exchange rate flexibility (only as one of the measures), the liberalization of both land and energy markets, and the rigorous implementation of environmental protection policies.

China's large external sector imbalance is a product of incomplete economic reform. The best way to reduce the imbalance is to finish the task of economic reform. The growing risks, including large current account surpluses, suggest that liberalizing factor markets should now be placed at the top of Chinese policymakers' agenda.

Yiping Huang is professor in the Chinese Center for Economic Research at Peking University and in the China Economy Program at the ANU.

{kind=link}

{kind=link}