China’s economy grew at 6.6% in 2018, according to official data – still impressive by global standards but slow by its own measures. The slowdown is the worst since the global financial crisis a decade ago, according to some analysts. How do we explain this? Let me try to put the slowdown of the growth drivers in perspective.

First of all, the slowdown validates the growth proposition -- the bigger one gets, the harder one grows. Indeed, 40 years ago China’s share of the world’s total GDP was about 2 percent; since then it has grown to about 15 percent. Now China (with about 13 trillion U.S. dollars) is already the world’s second-largest economy, although its GDP per capita (approaching $10,000) is still below the world’s average (about $12,000). Bad news and good news. A relatively low per capital GDP indicates growth potential for a catch-up economy. Look at urbanization rate. Having come up from 18 percent 40 years ago, China is now at about 55 percent -- compared to 80 percent for many advanced countries.

Put China’s growth rate in still broader perspective. For the math-savvy, imagine two regression lines: Starting from a low base of mere 156 U.S. dollars 40 years ago, one line has regressed steadily upward toward the world’s average level of GDP per capita (about $12,000). In the process of catch-up, growth rates were extraordinary – yes, double digits at times. Now as China approaches that level (indeed, some provinces have already surpassed it – e.g., in 2018 it was about $16,000; 15,000; and 13,000 for Jiangsu, Zhejiang, and Guangdong respectively, all with urbanization rate over 65%), the other line will regress downward toward the world’s average economic growth rate of about 3 percent (average 3.2% in the 1980s and 2.5% in the 2010s, according to the World Bank). So no surprise to me should China’s growth rate creep further down below 6% beyond 2020.

Secondly, unintended though, the slowdown may also be due to the central government’s efforts to contain pollution and fend off financial risks – two of the three on-going “campaigns” in China, i.e., on the environment, systemic financial risks, and poverty alleviation.

On the environment front, during my recent trips to the southern and interior parts of China, local officials informed me that many businesses had to close down due to tough pollution crackdowns imposed by the central government. Local entrepreneurs told me that while they are for the environment, they desperately need time to adjust and adapt to new pollution-control standards. The top-down, one-size-fits-all approach has hurt them badly.

On the financial front, primarily due to previous excessive macro-economic stimuli and expansionary measures via local government financial vehicles, China’s debt-to-GDP ratio – the combined leverage of households, companies and the government -- stands high, over 250 percent in 2018 (as compared to 180 percent for emerging markets) – a steep rise from 150 percent of GDP in 2008.

And in recent years the country has been trying to deleverage. Measures to defuse risks include using administrative fiat to aggressively crackdown on (rather than better regulate) the burgeoning shadow banking businesses (much of which, reportedly, ended up with “money-making-money”, so to speak, without reaching the real economy). Theoretically, deleveraging -- especially the type that purportedly aims to get rid of zombie firms – could, through what Schumpeter calls “a gale of creative destruction”, benefit the economy in the long run.

But in reality, as private entrepreneurs complained to me, “bad money drives out good ones”, so to speak -- scenarios that one cannot rule out given the mixed nature of the Chinese economy where state-owned enterprises (SOEs) continue to enjoy many privileges that private firms do not, e.g., in receiving bank loans. The crowding-out effect, they claimed, was particularly strong on the downstream of industrial value chain; and would have been less severe, had SOEs not monopolized the upstream and simply passed costs to the downstream where much of the non-state sector live. Increasingly being “sandwiched”, some have moved overseas (e.g., to Southeast Asia) for cost considerations.

While operational details remain elusive, aggregate numbers are telling. Whereas China’s non-state sector contributes more than 50 percent of the country’s tax revenue, more than 60 percent of GDP, more than 70 percent of technology innovation, more than 80 percent of urban employment, and more than 90 percent of job growth, it receives only 20 percent of bank loans; the rest goes to the state-sector, which is responsible for about 5 per cent of innovation. These numbers clearly indicate a deep structural problem that must be addressed at a time when China has to take innovation and entrepreneurship seriously.

And the fact remains that indirect financial (i.e., via bank loans) -- rather than direct financing (i.e., via stocks and bonds) -- still dominates China’s financial system (i.e., over 70%), and is the only tool for many SMEs. In other words, capital markets (not money markets), improved or not, are largely inaccessible and irrelevant to them.

Look still deeper. Financial repression – a political-economic term used to describe policies in China that result in low returns on savings and cheap loans to companies and governments -- has clearly favored less efficient and oftentimes sclerotic SOEs in capital allocation, thus causing the efficiency of the overall economy to have declined over time, and escalating systemic financial risks of late.

Thirdly, the trade spat between the United States and China, coupled with a lackluster global economy, has also helped dampen China’s growth by denting business and consumer confidence.

The auto industry, for instance, has been a major driver of China’s economic growth for years and an important barometer of Chinese consumers’ willingness to open their wallets. Its sales take up about 10 percent of the country’s total retail sales. With uncertainties surrounding the on-going U.S.-China trade disputes and negotiations, of which tariffs on auto imports are a sticking point, auto production in China declined in 2018 by 4.16 percent, with the December number down dramatically over 18.39 percent year on year.

Similarly, auto sales also contracted in 2018 (-2.76%), with the December number down over 13.03 percent year on year, according to the China Association of Automobile Manufacturers.

And all of this has happened against the backdrop that, since the world financial crisis in 2008 China has been trying to rebalance from an export-driven and resource-heavy growth model toward a consumption- and services-oriented model. Impressive progress aside (e.g., export-to-GDP ratio has pushed down from 30% in 2007 to 15% in 2018), this transition -- in essence from quantity to quality -- is still underway, and by no means pain-free, especially when China seems to have already reached the Lewis turning point, where surplus rural labor exhausts, causing wages to rise rapidly.

By the end of 2018 the service sector grew to more than half of the Chinese economy. Private consumption, however, was still less than 40 percent GDP, as compared to close to 70 percent for many advanced economies (e.g., 67% for the U.K. and 68% for the U.S.). Presumably, high housing price cuts consumption, as household debt-to-GDP ratio climbed up rapidly (by over 15 percentage points in the last 8 years). And yes, there has been much talk about new energy, new material, automation, bio-tech, Iot, AI, etc., as new growth drivers, but much of it is still on the horizon.

In short, growth of new industries and domestic consumption have been less than anticipated to offset the decrease in exports as well as in fixed investment due to overcapacity in old industrial and real estate sectors.

What should Chinese policymakers do in the face of the headwinds?

As growth decelerates, China should dynamically rebalance between growth and financial risks, as well as environmental concerns. This is because poor growth would worsen financial stability and vice versa. Understandably, balancing among and toward multiple targets of “reform, stability and growth” under conditions of internal and external uncertainty is by no means easy. One has to be constantly alert to both “grey rhinos” and “black swans”, so to speak, all along the way.

Internally, the country’s 1.4 billion population (17.9% of which are aged at and above 60 years old in 2018) is not just aging but about to decline over the coming decades with a low fertility rate of 1.6 (for perspective, 1.8 for the U.S. and 2.33 for India). And there are reports that deaths already outstripped births in 2018.

Externally, one big “grey rhino” is the rising tension between China and the United States -- trade being just part of the story -- made worse when hijacked by nationalist passions. Depicted as a “Thucydides’s trap” by Graham Allison of Harvard University, it represents a dangerous course that policymakers could, one hopes, only manage to reverse through extraordinary imagination and statecraft.

On December 1, 2018, at the G20 meeting in Buenos Aires, over escalating trade dispute Chinese President Xi Jinping and U.S. President Donald Trump, met and agreed to a tariff truce of 90 days to negotiate for a trade deal hopefully agreeable to both sides. What is its prospect? I am cautiously optimistic as long as the dialogue continues. Interests are not just “out there”, as constructivist scholars of international relations would advise, they are “constructed” in interactions. Which, to me, presumably is more plausible in economic than in political or security realms.

On December 21, 2018, at the annual Central Economic Work Conference chaired by President Xi Jinping, China’s leadership noted that “external environment is complicated and severe, and the economy faces downward pressure,” and they urged to “increase the sense of urgency”. It was clear from the statement of the meeting that arresting the slowdown would be a priority for 2019.

In response, Chinese policymakers have called for a “proactive fiscal policy,” including tax cuts, and urged a “prudent monetary policy” that is “neither too tight nor too loose,” indicating that China’s efforts to rein in escalating debt levels may be wound back slightly, in part to ease credit crunch. In other words, deleveraging would have to pace and calibrate well enough to include counter-cyclical measures.

In particular, the government has set up a lending program of 15 billion U.S. dollars specifically earmarked for entrepreneurs and small and medium enterprises (SMEs). With a tepid CPI inflation (2.1% in 2018) in evidence, and in light of China’s track record of macroeconomic stabilization, I would also expect a combination of stimulus measures, including further tax cuts, monetary easing (hopefully better tailored this time to reach where it is most needed), and fiscal spending (likely on more infrastructure projects, including social infrastructure) to follow in due course.

But this time the scope for policy maneuver is by no means large, because the excesses from 2008 and their hangover constraint options today.

Note, Chinese Premier Li Keqiang has sworn off what he calls “flood-irrigation stimulus”, a reference to the farming practice of soaking all the soil, not just the crops. The other thing China will try to avoid is a significant change to its property policies, a crucial part of the stimulus in 2008 that many believe has subsequently caused bubbles. Note also, Chinese President Xi Jinping has repeatedly said that homes are for living in, not for speculating on.

Indeed, China faces the so-called “risky trinity” (i.e., climbing debts, declining productivity and thus diminishing policy flexibility), and policymakers would also have to be watchful of the Phillips Curve – a macroeconomic notion of the trade-off between inflation and unemployment.

Having said that, however, I would also argue that it would be inadequate to deploy short-term stimulus measures to address the root causes of downward economic pressures now increasingly building up in China. Lest one forget, total factor productivity (TFP) has remained anemic for years in China, and productivity, at the end of the day, is the fundamental engine of sustainable growth.

While stimulus measures are necessary to prevent a deeper decline in the short term, thus temporarily boosting confidence and winning breathing space to address long-term concerns, China urgently needs a new round of supply-side structural reforms not only just at the level of policies but also at the more fundamental level of institutions.

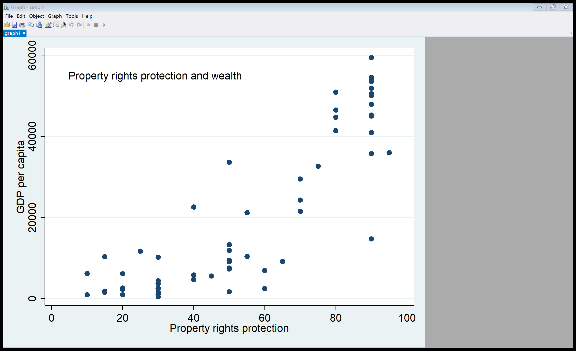

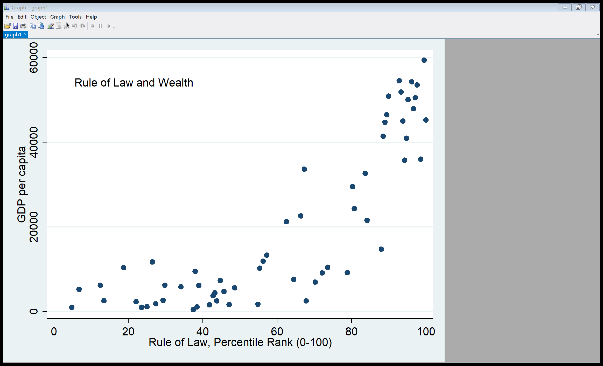

That is, in the mantra of “technology, innovation and entrepreneurship,” one should also heed the imperative of the institutional context that nurtures these critical variables. The real focus, therefore, must be on “letting the market play a decisive role” in resource allocation, including financial resources, and at the same time on “building the rule of law”, such that China is better positioned to roll back a plethora of administrative monopolies (such as in energy, logistics, telecom, finance, and land) that have often stifled rather than inspired innovation and entrepreneurship.

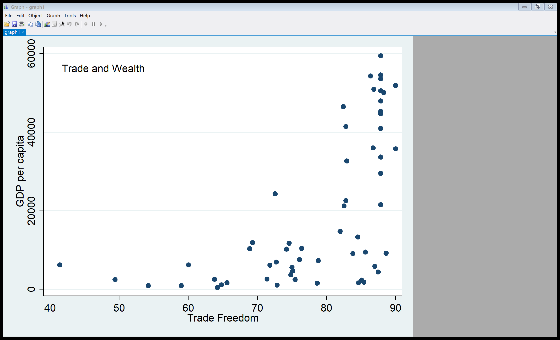

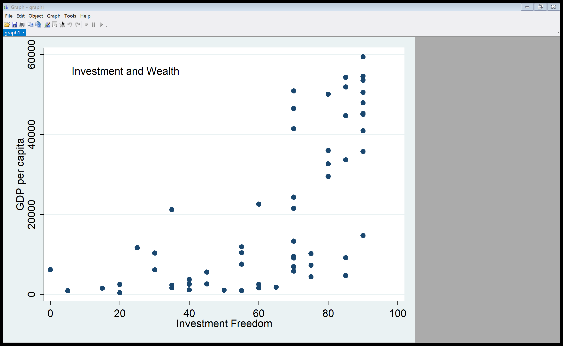

Accordingly, policies that further facilitate trade (including services) and investment openness and optimal resource allocation in an orderly manner are the right moves (see scatterplots in appendix), and if institutionalized, they could not only help ameliorate external tensions (e.g., especially with the U.S.), but also add exogenous impetus to supply-side structural reforms domestically.

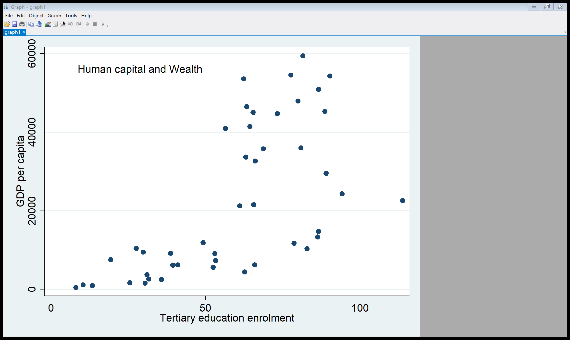

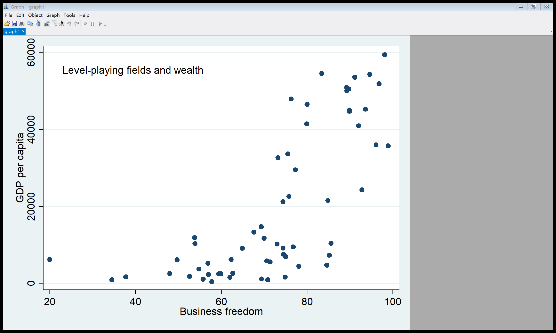

The reform agenda also has to involve deeper educational, healthcare, and SOE reforms. For, put in a global perspective, evidence is compelling, according to our analyses (see scatterplots in appendix), that growth toward and beyond the world average performance (about $12,000 per capita) would require enhanced institutional quality broadly conceived, e.g., human capital formation, level-playing fields, secure property rights, and the rule of law. And compared with these intangible assets, tangible physical capital would increasingly become less important as a driver of growth. To illustrate, look at electricity. Its consumption per capita in advance economies was near-zero growth in recent decades.

In short, beyond physical capital, institutional capital -- intangible though -- has to rev up and deepen for growth to continue in a sustainable fashion.

Looking ahead, China should redouble its efforts to build these intangible assets as long-term growth drivers. For, without which, the mere exercise of macro-economic stabilization and stimulus tools would only end up adding huge costs to the future – a point validated by China’s own recent experience of mounting debts and financial risks. But unlike fiscal spending whose effects are direct, institutions – invariably having to involve politics, economics and more -- take a long time to build. And that, paradoxically, makes the job all the more urgent.

------------------------------------- Appendix: regression results --------------------------------------

Note: The regression results are based on data from the World Bank, OECD, World Governance Indicators, and my own database